Daily Market View: Away We Go Again

1-Minute Market Rundown

- Equities have continued their bear market rally in recent weeks, however with inflation remaining elevated, and growth continuing to slow, gains could be short-lived

- In FX, this environment should support the dollar, despite the buck’s recent downtrend, with European currencies especially vulnerable

- Looking ahead, a busy slate of UK data, as well as the latest FOMC minutes, highlight this week’s economic calendar

- I’ll be discussing this, and more, in a live briefing at 8:30am London time; join the call here

Away We Go Again

Right, I’m back; here we go again, then.

Rested? Ya. Relaxed? As much as I ever am. Ready? I guess so…

I wrote the bulk of this note on (or in, depending on your point of view - that’s a running internal debate!) the plane back from LA, and must say that in-flight Wi-Fi is a technological marvel. The in-flight bar is also a marvel, where one did indulge in a lovely Napa Pinot Noir, so please forgive any typos!

On that subject, here’s a few other holiday takeaways - Northern California is much nicer than Southern; give me San Fran over LA any day of the week, even if the east coast is better overall; a fair few folk stateside could do well to learn the difference between an English and an Aussie accent; and, lastly, America’s well-reported problem with both drugs and homelessness is sadly all too evident, much more so than when I last visited prior to the pandemic.

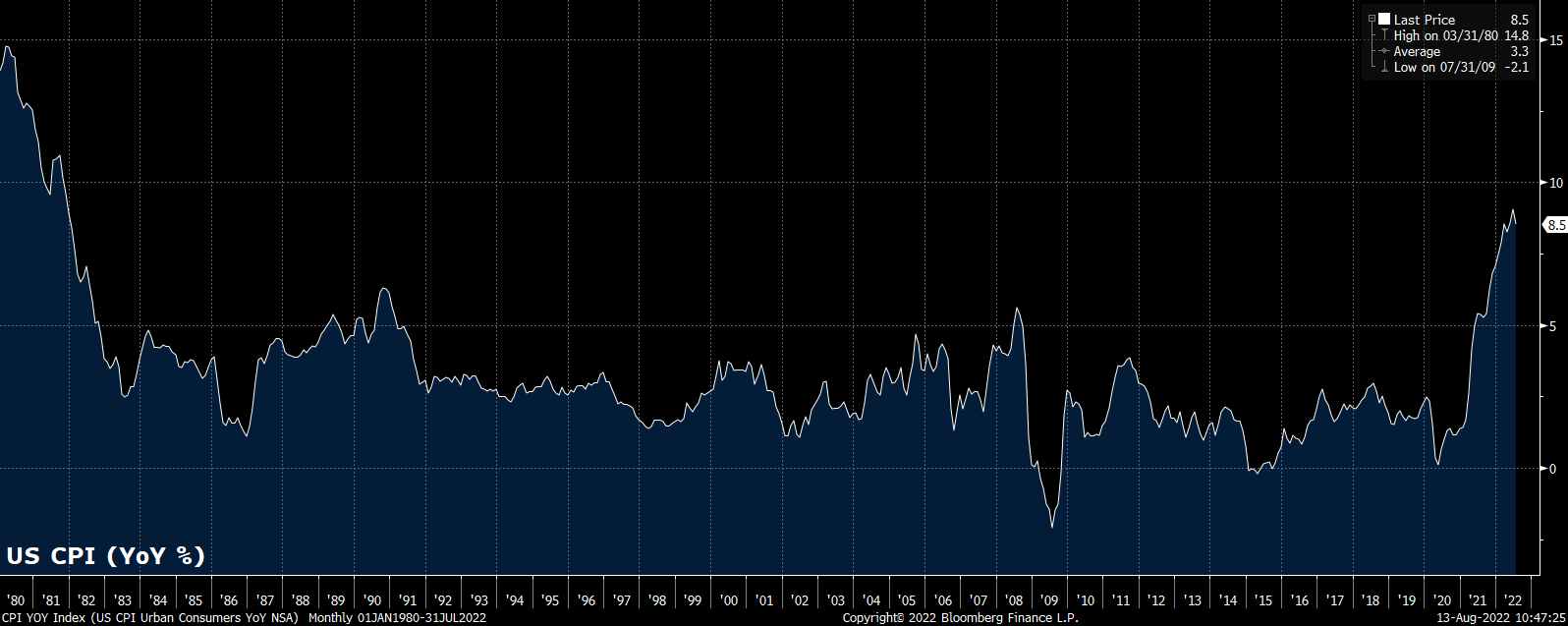

As for the markets, a lot has happened, but at the same time not much has changed, while I’ve been away. The US labour market remains surprisingly resilient, adding over half a million jobs in July, despite economic momentum continuing to wane, and inflation remaining elevated. Yes, CPI did moderate to 8.5% YoY in July, however this is still 4.25x the FOMC’s target - if anyone thinks that will get the Fed to pivot, then I have many bridges to sell you. Don’t even get me started on the Biden Administration’s claims that inflation was “0% in July” - watching US cable news channels cover that was enough to drive anyone insane.

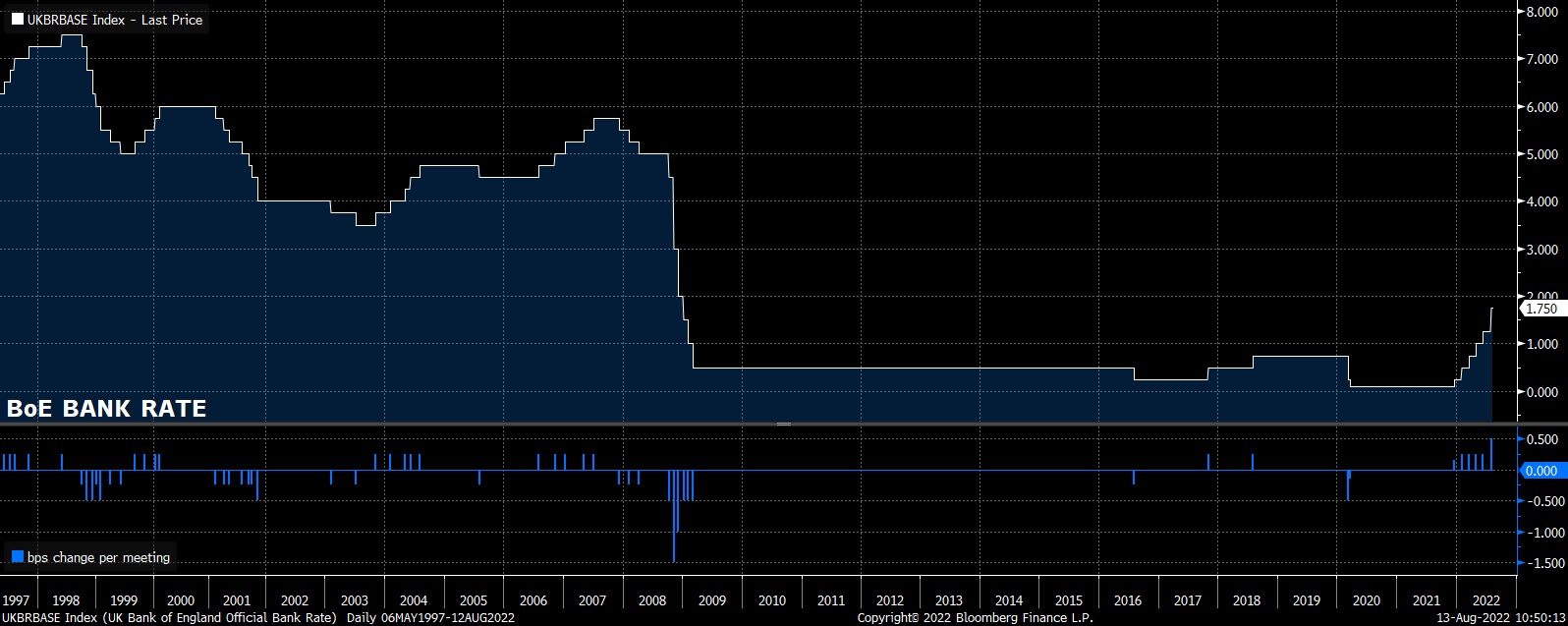

It was pleasing, though, while I was away, to see the BoE finally pull their finger out, with the ‘Old Lady’ hiking Bank Rate by 50bps for the first time since independence was granted in the late 90s.

This action was necessary, and also long overdue. However, it’s also far too little, far too late. I shan’t turn my first note back into a(nother) rant about the BoE, however with the Monetary Policy Report forecasting an inflation peak above 13%, as well as 5 straight quarters of recession, I struggle to see how anyone can be bullish on the UK economy, or on the pound - selling sterling rallies, taking cable back under 1.20, is still a favoured strategy of mine. Oh, I’m so glad I’ve flown back!

Things remain pretty grim in the eurozone; at least the UK isn’t suffering alone. It remains likely that the winter will bring severe energy shortages, for which the bloc remains underprepared. With the ECB hiking pretty aggressively (another 50bps next month) into this crisis, which will of course severely stunt economic growth, the euro’s fortunes look as bleak as the pound’s.

Clearly, central banks’ primary concern remains taming the inflationary beast that has been unleashed post-covid. If taming this tiger, to quote former BoE Chief Economist Haldane, requires destroying demand to the degree that a recession is caused, this is a price that policymakers are happy to pay. Frankly, they have no choice.

Subsequently, I find the remarkable rally in equities since I departed quite surprising, and still view the move as a bear market rally, rather than the beginning of a more sustained upswing. As I have mentioned on numerous previous occasions, I struggle to envisage a longer-lasting change in the market’s mood until the Fed pivot to a more dovish stance. >8% inflation will not permit such a pivot, even if investors are rushing to price it in as we speak. I’d expect Fed officials to toe a line similar to this at the Jackson Hole Symposium towards the end of the month, so perhaps stocks have a couple of weeks to continue rallying before then.

I’ve left the bond market until last in this whistle-stop market tour, though should perhaps have covered it first, as it’s the market which seems to make the most sense right now.

Front end yields keep pressing higher as the Fed lift overnight rates, while the long end dips (albeit remaining within a months-long range) as recession risks grow. All this causes the curve to invert deeper, and deeper, and deeper. Unless you think the US, and everywhere else, is going to suddenly see a massive pick-up in growth, coupled with a huge subsiding in geopolitical risk - I envisage neither - then it’s tough to bet against these trends continuing.

And so, another week begins. I reckon the next two weeks will be ‘proper’ summer markets, with a relatively quiet calendar, and relatively little market movement - famous last words, I hope not! This week’s contains relatively little of interest, besides minutes from the July Fed meeting, as well as the latest UK inflation and retail sales reports.

Fundamentally, we remain in an inflationary risk-off market, which is experiencing a bear market rally. Some think that the risk aversion has come to an end, however I do not, and expect a turning point relatively soon. Timing such a turning point is the tricky part, especially in this environment - no news seems to be good news, for now, so perhaps we shall have to wait for the fedspeak bonanza in Wyoming at the end of the month before it takes place. Either way, buckle up, bumpy times are ahead.

Today's Economic Calendar

No notable releases due.

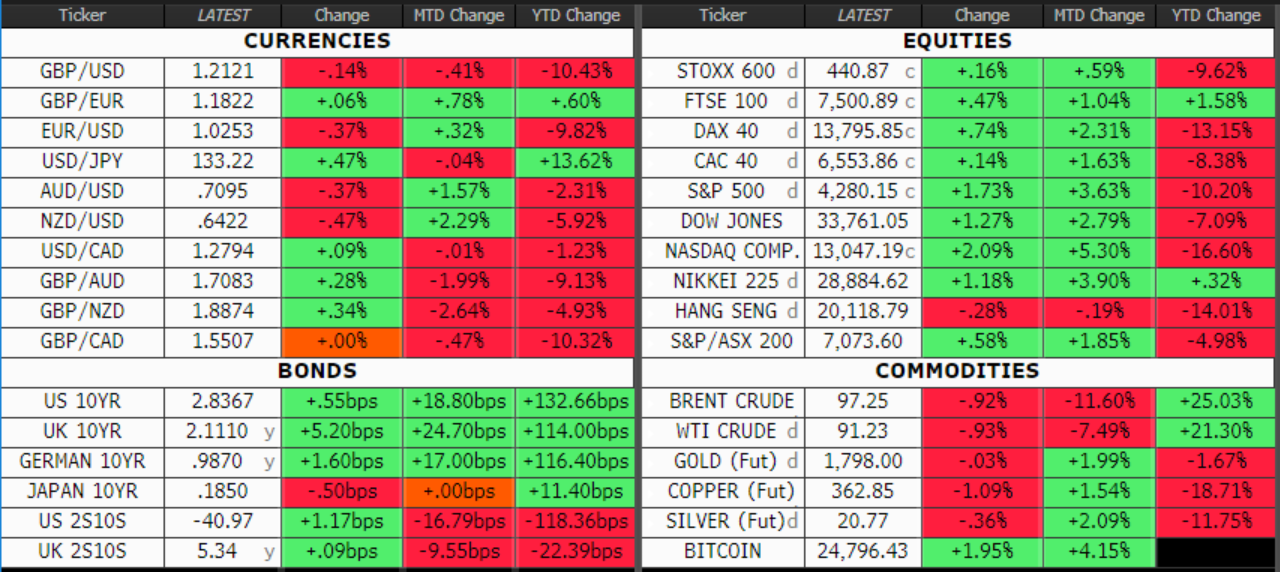

Markets This Morning (at 6am, London time)

I'd love to hear your comments, questions or suggestions. You can reach me on email at michael.brown@caxtonfx.com.

About the Author

Michael Brown is Head of Market Intelligence at Caxton, leading Caxton’s analysis, forecasting, and thought leadership within all areas of financial markets. He provides regular cross-asset market commentary and analysis, along with insight on market-moving macroeconomic events, being regularly quoted in national and international media. In addition, Michael leads on the inclusion and implementation of market research into Caxton’s data-led sales and marketing process. Away from Caxton, Michael is currently pursuing an Executive MBA at Cranfield University.

Share this article