Daily Market View: Markets Tread Water Ahead Of Fed Minutes

1-Minute Market Rundown

- Markets had a rather dull day yesterday, with relatively little major movement, and trading conditions becoming rather turgid

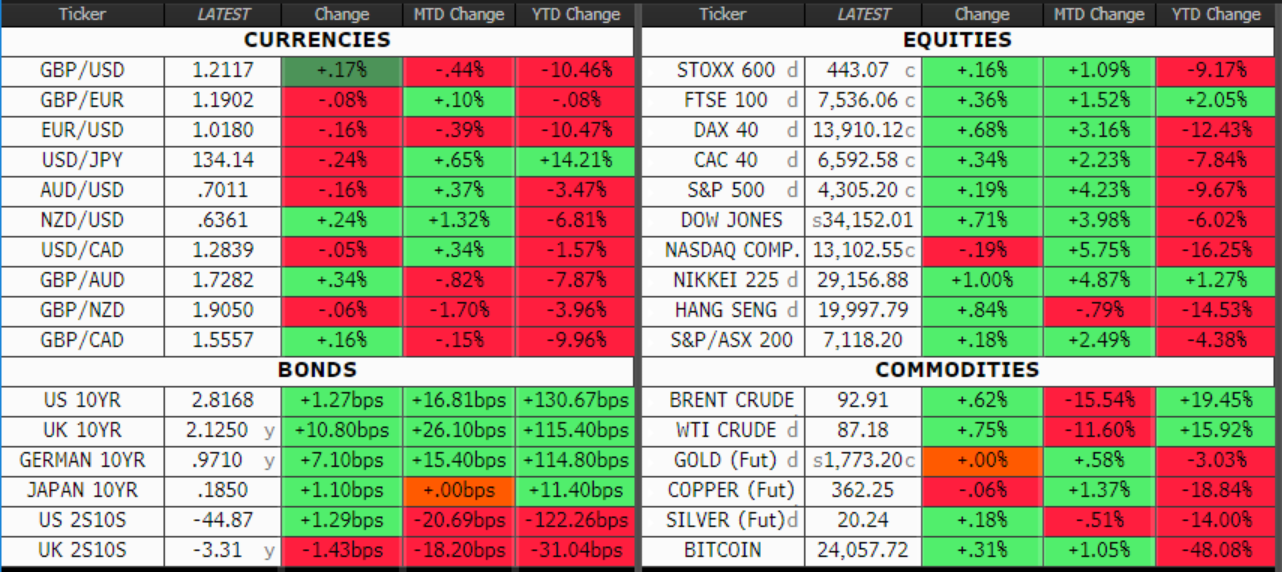

- In FX, things were similarly subdued, with the dollar flat against its peers on the day, and volatility continuing to fall across the board

- Looking ahead, minutes from the July FOMC meeting will be today’s main event, as well as revised eurozone growth data

Markets Tread Water Ahead Of Fed Minutes

Well, yesterday was a bit dull, wasn’t it?

As expected, not much happened, with markets seemingly in something of a holding pattern ahead of today’s FOMC minutes, and even perhaps ahead of the Fed’s Jackson Hole Symposium at the end of this month. You’re going to hear me mention that a lot in the coming weeks, as that’s the only interesting/exciting event in the near-term.

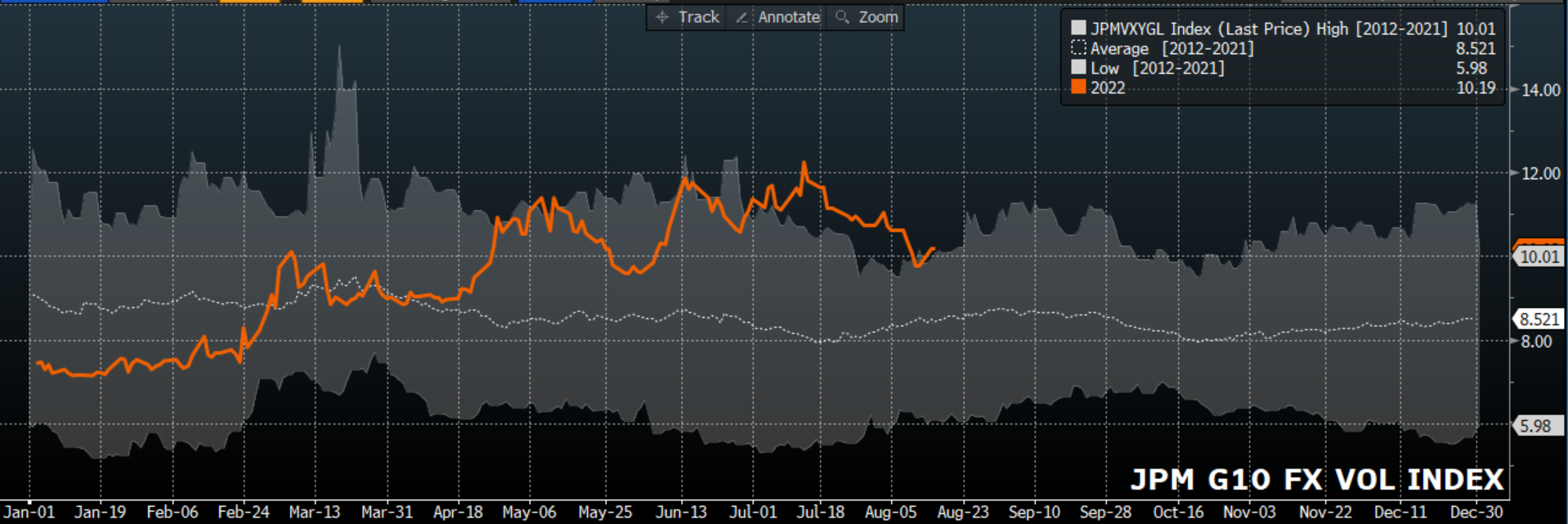

It’s not especially surprising, then, that G10 FX volatility has come sharply lower in recent months, as measured by JPMorgan’s proprietary index. Still, we remain well above the average level for this time of year, and are entering a period where vol tends to increase, and with Jackson Hole on the horizon, buying vol now might be a decent bet.

Something else that could, perhaps, contribute to elevated vol is the Tory leadership race, something which has started to grow rather tedious.

Nevertheless, it’s interesting that the market is almost totally ignoring the possibility of a Prime Minister Truss tinkering with the Bank of England’s mandate. While we are, as yet, unclear as to what form such tinkering could take, a shift back towards targeting the UK money supply, or even a move to add a nominal GDP target to the Bank’s remit, could both dent market confidence towards the UK economy, and British assets.

I guess we can add this to the list of bearish GBP drivers; I still think cable will trade sub 1.20 again in the short term. Throw the record fall in real pay seen in July onto that list as well, by the way.

On a different note, equities remain interesting, with the S&P having a look at its 200-day moving average yesterday, as the recent rally continued. The latest round of retail earnings were the primary catalyst behind the gains, with figures from giants including Walmart beating expectations, somewhat allaying investors’ concerns over the detrimental impact that surging inflation may have on consumer spending.

What stocks appear to be doing at the moment is pricing a scenario that is still pretty grim (high inflation, slowing growth, rising rates), but not quite the worst case stagflation/deep recession picture that most envisaged just a few months ago. It’s certainly not a ‘goldilocks’ situation, more of a ‘we’ve escaped the worst and that’s enough reason to buy’ one that is fuelling the gains.

And so, the busiest (probably) day of the week is upon us. This evening’s FOMC minutes will be the key event, with market participants looking primarily at two things; where the Fed view the terminal rate as likely sitting this cycle, and how members’ views on the growth outlook may influence their view on policy loosening 12-18 months from now.

Today's Economic Calendar

Markets This Morning (at 6am, London time)

I'd love to hear your comments, questions or suggestions. You can reach me on email at michael.brown@caxtonfx.com.

About the Author

Michael Brown is Head of Market Intelligence at Caxton, leading Caxton’s analysis, forecasting, and thought leadership within all areas of financial markets. He provides regular cross-asset market commentary and analysis, along with insight on market-moving macroeconomic events, being regularly quoted in national and international media. In addition, Michael leads on the inclusion and implementation of market research into Caxton’s data-led sales and marketing process. Away from Caxton, Michael is currently pursuing an Executive MBA at Cranfield University.

Share this article