Daily Market View: Recession Arrives

1-Minute Market Rundown

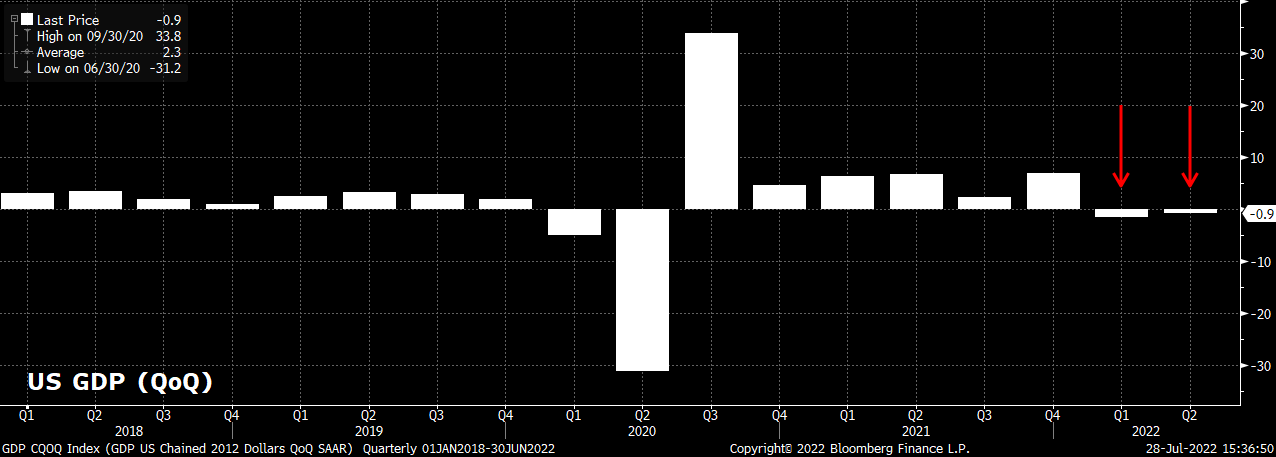

- Yesterday’s US GDP report confirmed that recession has arrived, with two consecutive quarters of negative growth having now been chalked up

- Markets, however, largely shrugged this off, with the bad news largely priced in, though both Treasuries and the JPY did stage impressive rallies

- Looking ahead, the week wraps up with a busy eurozone calendar, including the latest growth and inflation figures

Recession Arrives

I said yesterday that the Fed are now done & dusted for summer; I am also now done & dusted for a couple of weeks, with today being my final note until mid-August as I take a couple of weeks holiday.

Unfortunately, I must deliver some rather dismal news in my final note before departing. The US economy has now entered recession, with the economy having shrunk by 0.9% annualised QoQ in the second quarter, marking back-to-back quarterly contractions.

Now, there is some debate about whether we are actually in recession, with some pointing towards the resilience of the labour market (~400k monthly payroll gains are still being chalked up) as a reason to say that we are not in such a situation.

To them, I would suggest a quick browse of a nearby dictionary. I tend to find it easier to deal objectively with facts – when the definition of a recession is two consecutive quarters of economic contraction, and we have indeed seen said two quarterly contractions, we can safely say that this is now a recession.

If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.

This particular duck, however, appears to have been pretty well priced in by markets, given the lack of any significant reaction to the figures. I guess there are a few reasons for this – the report won’t change the Fed’s stance; a huge chunk of the negative impact on growth was caused by surging inflation; and, the fact that whatever the US is going through, Europe is going to experience a much worse situation this winter. I remain bearish risk, but due to tighter policy, not due to the growth shock.

One of few things that did show a major move post-GDP was the JPY, which found some demand, taking USD/JPY below 135, and to a one-month low. Markets seem happy to look through the BoJ’s continued uber-dovish stance for now, though I question how long this position will last.

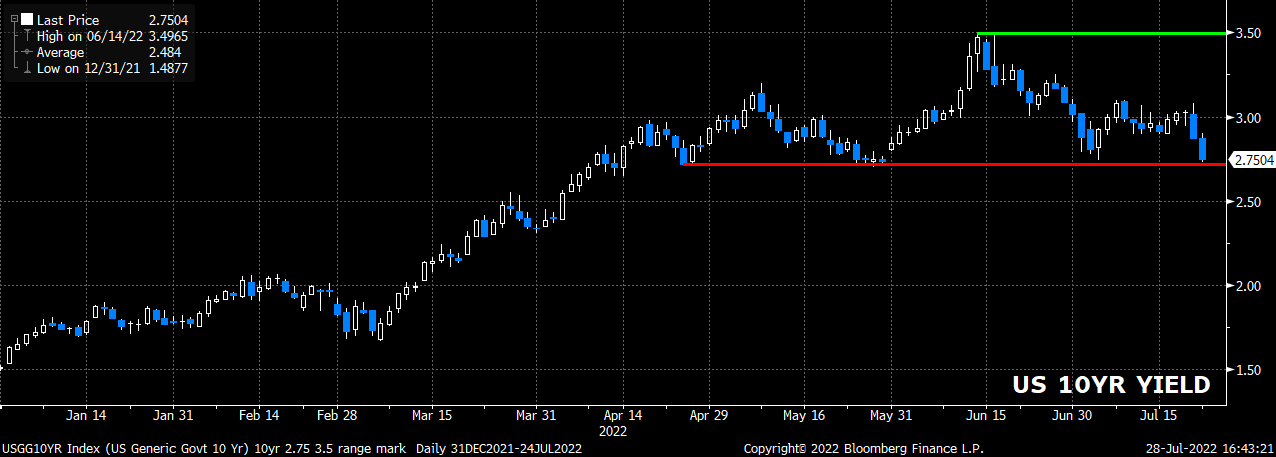

A big leg lower in Treasury yields, and further curve inversion, helped the JPY to catch a bid, including the 10-year Treasury touching its lowest level since 14th April. I wonder if bond bulls will now feel emboldened to take yields lower still, now that the recent range low has broken rather decisively.

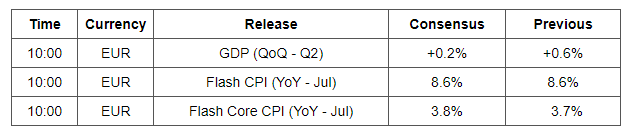

In any case, another busy day awaits today, with the latest eurozone inflation and growth figures highlighting the docket – the latter is likely to paint a similarly grim picture to the US report mentioned above.

I shall leave things there for today, and for the next two weeks. Thank you all for reading, and allowing me to take up 5/10 minutes of your morning every day. I’ll be back on 15th August, please try not to break the markets while I’m away.

Today's Economic Calendar

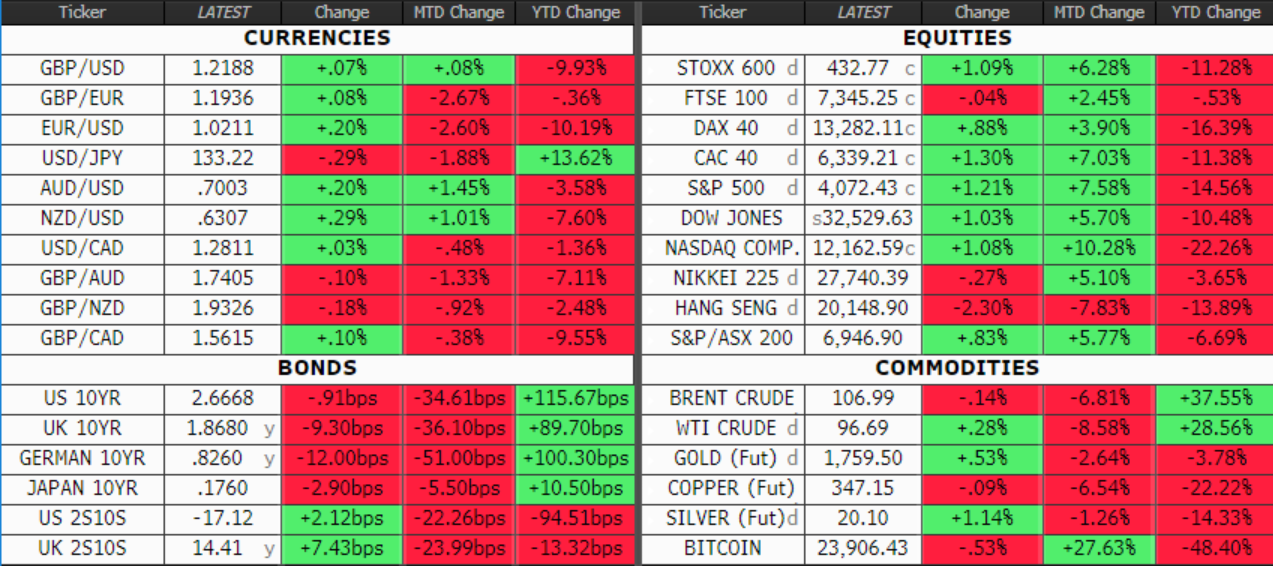

Markets This Morning (at 6am, London time)

I'd love to hear your comments, questions or suggestions. You can reach me on email at michael.brown@caxtonfx.com.

About the Author

Michael Brown is Head of Market Intelligence at Caxton, leading Caxton’s analysis, forecasting, and thought leadership within all areas of financial markets. He provides regular cross-asset market commentary and analysis, along with insight on market-moving macroeconomic events, being regularly quoted in national and international media. In addition, Michael leads on the inclusion and implementation of market research into Caxton’s data-led sales and marketing process. Away from Caxton, Michael is currently pursuing an Executive MBA at Cranfield University.

Share this article